[playht_player width=”100%” height=”175″ voice=”Noah”]

Coronavirus

It was the worst of times,

it was the best of times,

it was the age of uncertainty,

it was the age of information,

it was the epoch of isolation,

it was the epoch of technology,

it was the season of Darkness,

it was the season of Light,

it was the winter of despair,

it was the spring of hope,

Please forgive me, Charles Dickens, but twisting your meme slightly seems appropriate in this period of Covid 19. It’s difficult to speak of hope in the current context of losses of life, livelihoods, and institutions. And the uneven distribution of burden is so unfair. However, humankind is resilient. We are motivated by hope. Hence, perhaps a discussion of hope can be healthy in dark times. Following are 10 reasons why now is a good time to start your tech business.

1. Unparalleled Disruption

Future history books will mark the Covid 19 global pandemic not only as a landmark healthcare incident, but as a watershed event affecting daily life. We have already experienced massive changes in our modus vivendi – massive in impact, massive in personal scope, massive in global reach. Many changes are temporary, some permanent, some intentional, and many incidental – changes in healthcare, work, socializing, education, travel, recreation, shopping, eating. Humans are social beings, so the shorter list probably includes those rare activities unaffected by social distancing.

It’s entrepreneurial cliché that startup success can result in “disruption” to an entire industry (a la Uber to the taxi industry, or AirBNB to the hotel industry). But what if the disruption happens first? Many of the startup concepts that failed during the 2000 dotcom bubble have come to be today, from home grocery delivery (WebVan) to web-based spreadsheets (anyone remember Halfbrain.com?). There were multiple reasons for the dotcom collapse, but I would argue one key reason was that markets (people) were not ready for such rapid disruption.

The Covid pandemic has created the opposite situation, a tech “antibubble” or “globule” – a rapid disruption seeking solutions. Technology will often likely enable new solutions. Plus, most successful startups require creative ingenuity (e.g., for go-to-market). But, frankly, the tech is the less difficult part. Finding the burning unmet need is often the biggest challenge. Now, in a rare, perhaps (hopefully?) once-in-a-lifetime moment, a disruptive externality has produced many new needs. In essence, folks are longing for ways to get back to “normal”, at least doing the things that they love…but safely.

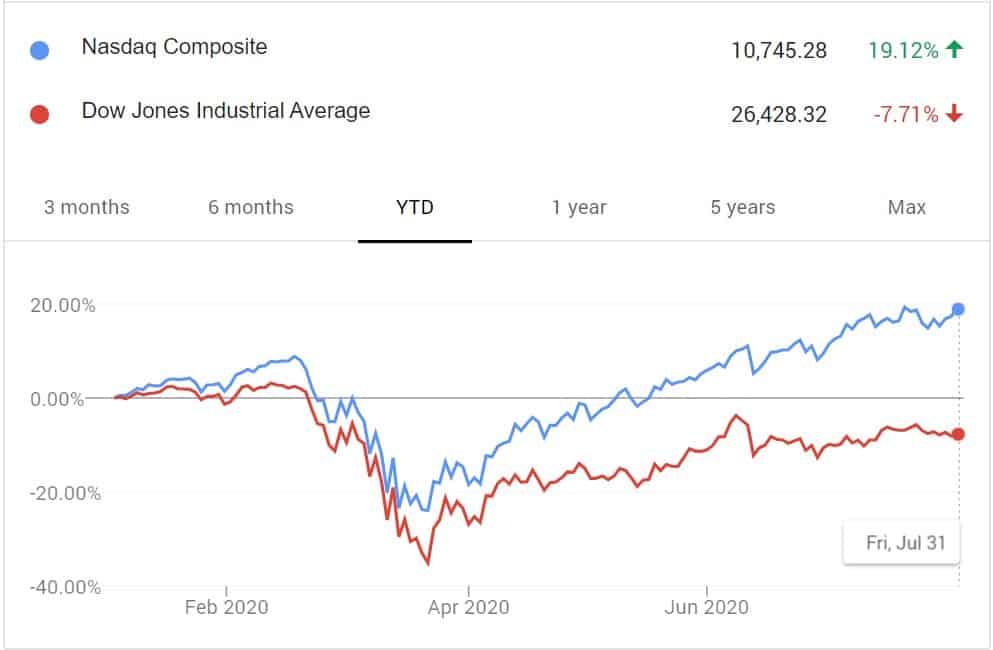

Many wonder why the stock market is “up” with such dire data, like depression-level unemployment. However, unemployment is a lagging result of an economic downturn. Again, the current situation is backwards with unemployment created by an externality. The stock market seems to agree. In fact, the increased spread between tech-heavy NASDAQ and the DOW illustrates a greater relative confidence in tech. Yes, in part due to tech’s resilience to social distancing, but also due to the new opportunities for tech companies. Case in point, Amazon just beat earnings estimates by 500%. And Macy’s CEO admitted that at least $10B of retail commerce is “up for grabs”.

(Google 7/31/2020)

“This is a greenfield pallet like we’ve never seen before for real entrepreneurs” – Ann Winblad, Hummer Winblad Venture Partners (Gener8tor webinar, 5/14/2020)

In fact, even from a macro perspective, technology growth curves have seemed to be impervious to economic downturns. For example, try to find the economic downturns in this exponential graph of the famous Moore’s Law:

2. Time Flexibility

Successful, now brand-name companies like Uber, Slack, Whatsapp, were born from the 2008 recession (see “5 Steps To Find Your Pivot During The Covid Crisis”)

We mustn’t glibly overlook the real hardships of many people. Loss of job, income, childcare can be devastating. It may not be possible, let alone interesting, for some to pursue starting a new business. But for those who can, some circumstances may be in their favor.

Many of us may be working less, commuting less, and have cancelled a lot of other personal activities…providing more time to put into a startup or learn new skills needed to start a business.

“We see there’s about $10 billion worth of opportunity that’s up for grabs right now based on what’s going on with the competitive climate” – Jeff Gennette, chairman and chief executive officer of Macy’s Inc. (CNBC, 5/21/2020)

3. Pressure On Buyers

Both in the consumer (B2C) and business (B2B) spaces, there is increased pressure to evaluate suppliers. Future uncertainty breeds financial austerity, which motivates buyers to not only be open to, but actively seek alternate suppliers to either reduce costs and/or to reduce supplier dependency risks. This can provide opportunities and an openness to receive even small startup suppliers.

4. Gig Talent

Just as you might, other people may have additional flexibility. Plus, they’re home with fewer outside activities; they’re more available. The rise of “gig” work now provides mature platforms for finding all kinds of talent globally to work on various short or long-term tasks. Whether you need help with design, programming, or legal, you can now easily find qualified individuals to assist on an hourly or project basis.

Check out: 99Designs, Fiverr, Freelancer, TaskRabbit, Toptal, Upwork, WeGrowth.

5. Team

Many top startup accelerators and investors will not invest in solo entrepreneurs. There’s good reason for this – e.g., complimentary skills, greater commitment, less key-person risk, larger network, etc. Chances are greater now that potential partners in your network may be available part or even full time. But even if you have no partner prospects, the good news is there are online resources to help you find one. Remember, instead of hoarding a large slice of a small (or nonexistent) “pie” (business), your chances are usually better when teaming up to build a bigger pie.

Check out: AngelList, CoFoundersLab, Founder2Be, StartupGrind, TechCofounder

6. Lower Costs

If, and this is yet to be fully seen in this external economic shock, prices of goods and services are forced down, it’ll be cheaper to launch your own business.

7. Remote Work

Remote, virtual collaboration platforms have received much attention by customers, which is motivating the platform developers to rapidly enhance their products making remote team work even easier and more effective.

Check out: Google Hangouts, Microsoft Teams, Vectera, Zoom

8. Fundraising

So far at least, the stock markets have rebounded. Individuals (including your friends and family) have hopefully retained, perhaps even grown their financial holdings. They may not want to risk putting more in the stock market, so might be open to supporting your startup. While venture capital investing is down, investments continue to be made even solely via virtual meetings.

9. Software Development

“Software is eating the world.” In fact, many non-software-based solutions (e.g., hardware products) require some software component. Mobile computing is making user access ubiquitous. While Open source and cloud computing have made it so much easier to develop and deliver software products. And, in fact, with the evolution of low code to now “no code” options, it has never been easier to create software solutions.

Check out: apprat.io, bubble.io, cloudworx, codeflow, enduvo, postscapes, thunkable, turbo systems, webflow

10. Less Competition

Sadly, not everyone will read this blog post, so most will make the mistake of not capitalizing on the unique opportunities at hand. Some existing startups will lose the cashflow “musical chairs” game and not survive. Incumbents with high expenses may be on the rails, optimizing for cash, cutting discretionary spending and R&D. That all means less competition for you.

Getting Started

“You have to see complexity and uncertainty as signposts of opportunity, and we certainly have lots of that right now.” – Ann Winblad (Gener8tor webinar, 5/14/2020)

1. Problem

The first question is: Do you have an idea? If so, skip to “Opportunity Evaluation” below. If not, the most likely place for ideas and the greatest chance for success is within your domain of experience. Everyone has areas in which they have experience that is significantly deeper than most others.

Sure, you may have an opinion about how to make the best blueberry muffins, or why scheduling group meetings shouldn’t be so difficult. But unless you have unique domain experience much deeper than most, you could end up wasting a lot of time and money. Instead, focus on solving problems in areas you know well.

By “problem”, I mean an optimization. Businesses are constantly trying to improve their earnings or valuation, so they tend to be receptive to solutions that generate revenue or cut costs. In the consumer space, is drinking beer solving a problem? Well, it is if you are trying to optimize for happiness, at least that’s what beer marketers will then try convincing you of.

If you have expertise with a new technology, that may enable you to solve problems in new ways. However, you still need the right problem to solve. So when you’re excited about and proficient with a tech, it’s often tempting to start implementing the tech at the first applicable problem encountered.

Again, without proper analysis of the problem, you could end up wasting a lot of time, effort, and money. Here are some key questions to answer before building your product:

- Is the problem perceived to be important enough by the customer to put time, money, and effort into fixing it? Selling breath mints to people with bad breath, who do not think they have bad breath, is a difficult slog.

- Is the market and profit big enough to sustain a business? If the profitability is low and need narrow, you may have enough for a lifestyle business (which is fine), but perhaps not a fundable one.

- How competitive is the market for solving this problem? Make sure you look at the status quo (how potential customers are currently dealing with the problem) very carefully.

- Are you the best to solve this problem long term? Or are there other better funded experts who are likely to provide a solution, especially after you show them there’s a market for it?

Successful entrepreneurs are maniacal about solving a customer problem that they understand better than most, not about a particular technology.

2. Opportunity Evaluation

Make sure you test your startup idea before investing in building a solution. Some of the USA’s greatest strengths include a structure and culture that encourage innovation. But this attracts a lot of people seeking to solve problems. Thus, it’s quite rare to find a problem to which someone has not already offered a solution.

Believe it or not, much of an investor’s (economic vs philanthropic) goals are probably well aligned with yours if you seek economic reward. “To Get Your Startup Funded, Answer These 3 Investor Questions in Your Pitch” provides a good framework for evaluating your startup business idea.

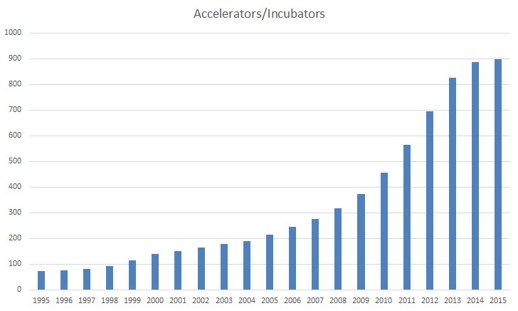

3. Accelerators

Of course, you can pursue your startup business on your own. Everyone has different skills and abilities. However, if you feel like your chances might improve with a little help, there’s good news. Plenty of startup accelerators (including incubators, etc.) have emerged over the recent years. Most will provide guidance, introductions, and sometimes investment.

(Pitchbook, 7/24/2015)

Many accelerators focus on domains, geographies, and/or technologies. If you need help finding an accelerator that’s right for your business, here’s a searchable database of over 400 global accelerators.

The best accelerators can be quite selective. For example, it’s not uncommon for one accelerator to receive hundreds of applicants for 10 open spots in a class or cohort. I help startups prepare to apply for accelerators. If interested in my help preparing to apply, click here.

I may be biased. I’ve lived in Silicon Valley for over 20 years. But Silicon Valley continues to be a global leader in building valuable startups. Not all successful founders are from Silicon Valley, but many at least come through Silicon Valley to start their technology business. Steve Jobs gives five great reasons why.

Following are a few top-tier accelerators with different focuses in Silicon Valley accepting new cohorts, but their application deadlines are upon us, so act fast:

- NASDAQ: Applications due August 2, 2020

- SOA (Sustainable Ocean Alliance): Applications due August 3, 2020

- UC Berkeley SkyDeck (team member must have an association with any University of California campus or be a foreign national): Applications due August 8, 2020

Starting a new venture can be exciting, exhilarating, frustrating, difficult to say the least. Don’t go into it lightly, but if you have the desire, now might be a great time. Either way, best of luck! Please ping me if I can be of any assistance: www.Ghosh.com

Leave A Comment